Dividend Shares From Scratch:

Why £25 A Month Is All You Need To Begin

Now, here is the part most beginners miss... you can begin buying dividend shares with as little as £25 a month. That is not a gimmick. It’s a direct consequence of fractional investing, something most UK platforms now support. This post is built around that single, liberating fact.

I’ll walk you through every practical step—what dividend shares actually are, why starting tiny is not just possible but powerful, and exactly how to buy your first one or two individual dividend shares without any prior knowledge.

No stock tips, no jargon, no unrealistic promises. Just a clean, actionable path from zero to income.

Now, here is the part most beginners miss... you can begin buying dividend shares with as little as £25 a month. That is not a gimmick. It’s a direct consequence of fractional investing, something most UK platforms now support. This post is built around that single, liberating fact.

I’ll walk you through every practical step—what dividend shares actually are, why starting tiny is not just possible but powerful, and exactly how to buy your first one or two individual dividend shares without any prior knowledge.

No stock tips, no jargon, no unrealistic promises. Just a clean, actionable path from zero to income.

What Are Dividend Shares?

A dividend share is a share in a company that chooses to pay out a portion of its earnings to its owners—the shareholders—on a regular basis. If you own such a share, you receive cash payments, typically twice a year for UK companies, though some pay quarterly or even monthly. Think of it like this... you put some money into a well-established business, perhaps a large British insurance firm or a FTSE 100 energy group. The company trades, makes a profit, and at the end of its financial period, the board decides to give some of that profit directly back to you. The payment arrives in your brokerage account as a dividend. You have not sold your stake. You still own the share. The income is yours to keep or reinvest.

The term shares and dividends often gets thrown around in the same breath, and for good reason. When you buy a share, you gain two potential sources of return... any increase in the share price over time, and the dividend income distributed along the way.

With dividend shares, I pay particular attention to the second part—because that income is tangible, predictable, and completely independent of whether the share price happens to be up or down on a given Monday.

Think of it like this... you put some money into a well-established business, perhaps a large British insurance firm or a FTSE 100 energy group. The company trades, makes a profit, and at the end of its financial period, the board decides to give some of that profit directly back to you. The payment arrives in your brokerage account as a dividend. You have not sold your stake. You still own the share. The income is yours to keep or reinvest.

The term shares and dividends often gets thrown around in the same breath, and for good reason. When you buy a share, you gain two potential sources of return... any increase in the share price over time, and the dividend income distributed along the way.

With dividend shares, I pay particular attention to the second part—because that income is tangible, predictable, and completely independent of whether the share price happens to be up or down on a given Monday.

Why Should I Invest In Dividend Shares With Just £25 A Month?

I have met countless people who believed that building a meaningful portfolio required thousands of pounds upfront. That belief kept them on the sidelines for years. The truth is far more encouraging... regular small sums, invested consistently into quality dividend shares, compound into genuinely significant sums over time. A monthly commitment of £25 is deliberately achievable. It is less than a streaming subscription and a couple of takeaway coffees. Yet if you direct that modest amount into dividend shares every month and reinvest the dividends you receive, you set in motion a compounding engine that grows steadily in the background. The psychological benefit is just as important as the financial one. Starting small builds the habit without fear. Once the habit is established, it is remarkably easy to increase the monthly contribution as your circumstances improve.

I started my own journey with an amount that felt almost embarrassing at the time. Today, that early discipline is the reason my portfolio generates a comfortable five-figure annual income. Nobody begins at the finish line. The key is simply beginning.

A monthly commitment of £25 is deliberately achievable. It is less than a streaming subscription and a couple of takeaway coffees. Yet if you direct that modest amount into dividend shares every month and reinvest the dividends you receive, you set in motion a compounding engine that grows steadily in the background. The psychological benefit is just as important as the financial one. Starting small builds the habit without fear. Once the habit is established, it is remarkably easy to increase the monthly contribution as your circumstances improve.

I started my own journey with an amount that felt almost embarrassing at the time. Today, that early discipline is the reason my portfolio generates a comfortable five-figure annual income. Nobody begins at the finish line. The key is simply beginning.

Can You Really Buy Dividend Shares For £25?

Yes, absolutely. The mechanism that makes this possible is called fractional investing, and it has quietly transformed the landscape for private investors in the UK. Until relatively recently, you could only buy whole shares. If a single share of a FTSE 100 dividend-paying company cost, say, £120, and you only had £25 to invest, you were priced out. You had to wait until you had saved enough for one full share, which could take months. Fractional investing changes that entirely. It allows you to buy a slice of a share—exactly £25 worth, or whatever sum you choose. If that £120 share is available fractionally, your £25 buys you roughly 0.208 of a share. You then own that fraction, and you are entitled to the same proportional dividend. When the company pays a dividend of, for example, £6 per full share annually, your fractional holding receives 0.208 times £6, or about £1.25 in dividend income over the year. It is not a rounding error; it is a real, proportionate ownership stake, and it grows as you add more month by month. This means your very first £25 can immediately purchase a piece of one or two individual, high-quality dividend shares. No need to save up hundreds. No need to settle for a fund that pools hundreds of shares together, though funds certainly have their place. You can start right now, buying a sliver of a real business that pays real dividends. For me, that is an extraordinarily powerful starting point.How Do I Actually Buy My First Dividend Share?

The practical process is simpler than most newcomers expect. I’ve distilled it into a handful of clear steps.1. Open a Stocks and Shares ISA

For almost every UK investor, the first move should be to open a Stocks and Shares ISA. Any dividend income you receive inside this account is completely free of UK income tax, and any capital gains when you eventually sell are tax-free as well. You can contribute up to £20,000 each tax year. I have used an ISA for over two decades and consider it the single most sensible account structure for a dividend investor.2. Select an investment platform that offers fractional shares

Several established UK platforms now offer fractional investing alongside regular monthly investing plans. Look for one that charges low or no commission on regular monthly purchases and supports fractional share dealing. You do not need a bells-and-whistles trading interface. A clean, reputable platform with strong customer service and ISA management is ideal.3. Set up a regular monthly instruction

Once your ISA is open and funded, you instruct the platform to invest £25 each month into one or two specific dividend shares. Most platforms let you set this up in under five minutes. The transaction happens automatically on a set day, and the platform purchases the appropriate fractional amount at the prevailing price. You genuinely do not need to watch the market or time your purchase. Automation removes emotion from the equation.4. Choose your first one or two dividend shares

This is the part that makes beginners nervous, but it does not need to be complicated. The next section walks through a straightforward selection approach.How To Pick Your First One Or Two Dividend Shares Without Any Guesswork

I deliberately avoid naming specific companies, because your circumstances and goals are unique. Instead, I’ll give you the filter I use myself when selecting a reliable dividend share. Apply this filter to any large, well-known UK business you already recognise from the high street, the energy sector, or the financial pages, and you will quickly narrow the field.Look for a business that has paid and grown its dividend for at least five to ten years.

A consistent payment record signals that the board prioritises shareholder returns. A decade-long track record of rising dividends is even better. Many large UK companies proudly maintain such streaks.Target a dividend yield that is generous but not desperate.

A sensible yield for a quality dividend share often sits between 2% and 4.5%. Anything approaching double digits warrants caution. I once chased an 11% yield early in my investing life and watched the dividend get halved six months later. A moderate, sustainable yield is far more valuable than a headline-grabbing one.Ensure the business is easy to understand.

If I cannot describe what a company does in two sentences, I do not invest. A large British insurance firm that underwrites policies and invests premiums is straightforward. A FTSE 100 energy business that produces and sells fuel is straightforward. A household-name telecommunications provider is straightforward. Stick to what you can explain to a friend over a cup of tea.Check that the dividend is comfortably covered by earnings.

While I promised no jargon, this one concept is worth learning... dividend cover. It simply means the number of times the company could pay its dividend out of its annual profits. A cover of 1.5 or higher suggests the payment is secure. Below 1.0, the company is paying out more than it earns, which is rarely sustainable. Most good platforms display this figure on the share’s factsheet. Generic examples to illustrate the point... ... A large British insurance and investment management group that has distributed a steady or rising dividend for over a decade, with a yield around 4% and solid cover. ... A FTSE 100 integrated energy business that generates substantial cash flow and has a long-standing policy of returning cash to shareholders, even as it invests in the energy transition. These are not recommendations, just illustrations of the type of companies I mean. You could start with just one of these types, or split your £25 between the two to gain instant diversification. The important thing is to own something you understand and feel comfortable holding for years.What Platform Do I Need To Buy Dividend Shares?

The UK investment platform market is competitive, which benefits beginners. You are looking for a provider that offers three things as a minimum...- A Stocks and Shares ISA wrapper

- Fractional share dealing so £25 buys a slice of a full share

- Regular monthly investing with low or zero trading fees.

What Happens After I Buy? Understanding Dividend Payments

Once you have purchased your fractional dividend share, the company begins working for you. The mechanics of dividend payments are refreshingly simple. Most UK dividend shares pay twice a year... an interim dividend and a final dividend. The company announces a payment per full share—say, 15 pence. Because you own a fraction of a share, you receive the same fraction of that payment. If you own 0.2 of a share, you receive 0.2 times 15 pence, or 3 pence. It arrives as cash in your ISA account.

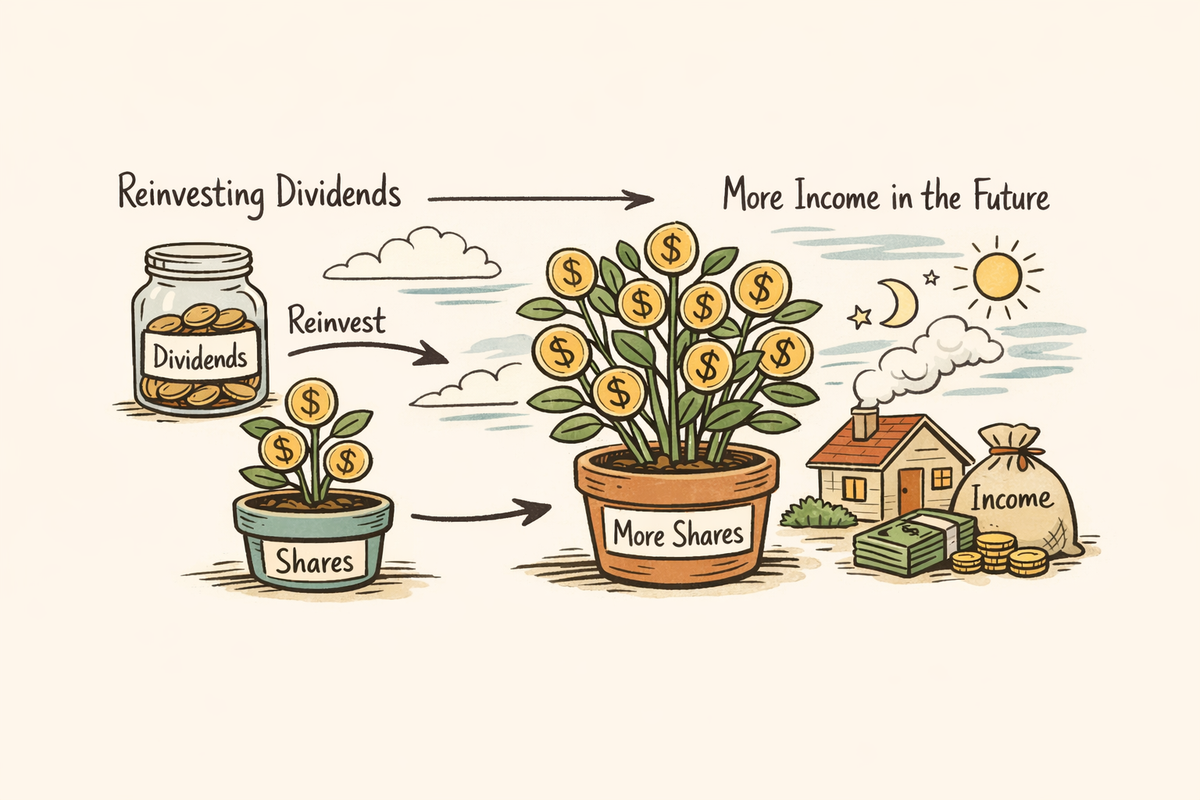

You then have a choice. You can leave the cash sitting in your account until you have enough to buy more shares manually, or you can activate automatic dividend reinvestment. With the latter, the platform uses your dividend income—however small—to purchase more fractional shares in the same company. This means your holding grows not only from your monthly £25 contributions but also from the dividends those shares generate. Even a few pence reinvested today becomes a little extra income tomorrow, and that cycle repeats ad infinitum.

There are a couple of key dates to understand, and once you do, you will never be caught out...

Most UK dividend shares pay twice a year... an interim dividend and a final dividend. The company announces a payment per full share—say, 15 pence. Because you own a fraction of a share, you receive the same fraction of that payment. If you own 0.2 of a share, you receive 0.2 times 15 pence, or 3 pence. It arrives as cash in your ISA account.

You then have a choice. You can leave the cash sitting in your account until you have enough to buy more shares manually, or you can activate automatic dividend reinvestment. With the latter, the platform uses your dividend income—however small—to purchase more fractional shares in the same company. This means your holding grows not only from your monthly £25 contributions but also from the dividends those shares generate. Even a few pence reinvested today becomes a little extra income tomorrow, and that cycle repeats ad infinitum.

There are a couple of key dates to understand, and once you do, you will never be caught out...

- Ex-dividend Date: The cut-off. You must own the share before this date to receive the upcoming dividend. Buy on or after it, and you wait for the next payment.

- Payment Date: The day the cash lands in your account.

The Magic of Reinvesting Tiny Dividends

If there is one concept I wish every beginner would internalise immediately, it is this... reinvest your dividends, especially when the amounts look laughably small. In the early months, your dividend income from a £25 investment might be a few pence. It is tempting to dismiss that as irrelevant. But those few pence buy you additional fractional shares, which then generate their own tiny dividends. The following month, your £25 plus the reinvested dividend buy slightly more. The month after that, slightly more again.

This is compounding in action, and it works best over long stretches. A dividend share yielding 4% and growing its payout by 3% annually, with all dividends reinvested, can double your total investment base in less than two decades without any increase in your monthly contribution. When you also gradually raise your monthly investment from £25 to £50 or £100 as your earnings grow, the effect is profound.

The challenging part is simply allowing the process to unfold without interrupting it.

I still have the records from my first year of investing. The dividend entries were comically small.

Today, those same holdings generate monthly income that would have covered my entire early portfolio several times over.

Patience is not just a virtue in dividend investing... it is the entire strategy.

In the early months, your dividend income from a £25 investment might be a few pence. It is tempting to dismiss that as irrelevant. But those few pence buy you additional fractional shares, which then generate their own tiny dividends. The following month, your £25 plus the reinvested dividend buy slightly more. The month after that, slightly more again.

This is compounding in action, and it works best over long stretches. A dividend share yielding 4% and growing its payout by 3% annually, with all dividends reinvested, can double your total investment base in less than two decades without any increase in your monthly contribution. When you also gradually raise your monthly investment from £25 to £50 or £100 as your earnings grow, the effect is profound.

The challenging part is simply allowing the process to unfold without interrupting it.

I still have the records from my first year of investing. The dividend entries were comically small.

Today, those same holdings generate monthly income that would have covered my entire early portfolio several times over.

Patience is not just a virtue in dividend investing... it is the entire strategy.

Common Pitfalls When Starting Small With Dividend Shares

I have encountered most of these traps personally, and I hope you can sidestep them entirely.Overcomplicating the selection of the first share

You do not need to identify the single best dividend share in the entire market. You need a good, understandable business with a sensible yield. Perfection is the obstacle to progress. Pick one or two solid names and begin.Monitoring the share price daily

Dividend shares are long-term holdings. The share price will move up and down—sometimes sharply. I check my portfolio once a month and rebalance once a year, not once an hour. Obsessive watching leads to emotional decisions, and emotional decisions are rarely good ones.Cashing out dividends too early

When you are building wealth, every pound of dividend income should be reinvested unless you have a specific, pre-planned need for the cash. Spending the income in the early years is like eating your seed crop. Keep planting.Ignoring the tax wrapper

Holding dividend shares outside an ISA exposes the income to tax once you exceed the dividend allowance (£500 for the 2025/26 tax year). Inside an ISA, you never pay a penny of tax on dividends or capital gains. It takes ten minutes to open an ISA, and the long-term benefit is enormous.Giving up because the early amounts feel trivial

This is the biggest pitfall of all. £25 a month does not feel significant. Six months in, the portfolio might still feel tiny. Twelve months in, the dividend income might only buy a modest lunch. But the trajectory is what matters. Every long-term successful dividend investor I know started with sums that felt negligible at the time. Consistency and time are the great equalisers.Frequently Asked Questions About Dividend Shares

What exactly are dividend shares?

Dividend shares are ordinary shares in companies that regularly pay a portion of their profits to shareholders. When you own them, you receive cash payments, usually twice a year for UK firms, simply for holding the shares.Can I really start buying dividend shares with just £25 a month?

Yes. Fractional investing allows you to buy a slice of a share for as little as £25. Many UK investment platforms support regular monthly fractional purchases, making it possible to own individual dividend shares without needing hundreds of pounds upfront.How do dividend shares pay me?

The company declares a dividend per share, and you receive a proportionate amount based on the number of shares or fractional shares you hold. The cash is deposited directly into your brokerage account on the payment date.Do I need a Stocks and Shares ISA for dividend shares?

While not mandatory, a Stocks and Shares ISA protects all dividend income and capital gains from UK tax. For most investors, it is the most tax-efficient way to build a long-term dividend portfolio.What is the ex-dividend date?

The ex-dividend date is the cut-off day for receiving the next dividend. You must own the shares before this date to qualify. If you buy on or after the ex-dividend date, you will receive the following dividend instead.Should I reinvest my dividends or take the cash?

In the early years of building wealth, reinvesting dividends is generally the most powerful strategy because it accelerates compounding. Taking the cash makes more sense once your portfolio has grown sufficiently and you need the income.How do I pick a good dividend share?

Look for a business you understand with a sensible yield (often 2 – 4.5%), a track record of stable or growing dividends, and dividend cover comfortably above 1.5. Avoid chasing the highest yields in the market, as those can signal an impending cut. Dividend shares are not reserved for the wealthy or the financially sophisticated. They are accessible to anyone willing to start small, stay consistent, and let time do the heavy lifting. I opened my first ISA with an amount that barely registered on a bank statement, and it became the foundation of everything that followed. The mechanics are simple, the barriers are lower than ever, and the long-term rewards speak for themselves. If you have been waiting for the perfect moment to begin, consider this your signal. Open a Stocks and Shares ISA, set up a £25 monthly instruction into one or two solid dividend shares, and reinvest every payment. The portfolio you build over the next ten years will thank you for the decision you take today.- Dividend shares pay you regular cash out of company profits, simply for owning a piece of the business.

- You can start buying individual dividend shares with as little as £25 a month using fractional investing inside a Stocks and Shares ISA.

- Select your first one or two dividend shares by focusing on familiar, understandable businesses with a sensible yield, a track record of steady payments, and comfortable dividend cover.

- Focus on dividend growth, not just today’s yield. A modest payout that rises year after year will outpace a static high yielder over time.

- Reinvest every penny of dividend income in the early years to harness compounding—the engine that transforms tiny sums into significant wealth.

- Automate your monthly investment and dividend reinvestment to remove emotion and maintain consistency.

- Keep your investment costs low. Even small platform fees compound, so choose a provider with competitive charges for regular, modest trades.

- Ignore daily share price movements. Dividend investing rewards patience, not frantic activity.

- Build the habit before increasing the amount. Consistent £25 monthly investments that become automatic are far more powerful than sporadic lump sums.

- Start today, not when you have “more money”. The most valuable asset a dividend investor possesses is time.

Return from Dividend Shares To Why You Need Dividend Investing For Stock Market Cash Flow