Ex-Dividend Dates Made Simple:

How To Time Your Dividend Income

And Keep More of What You Earn

But here’s the truth... once you’ve spent ten minutes with the idea, you’ll wonder what all the fuss was about.

Understanding the ex-dividend date is a bit like learning the offside rule in football. It feels impenetrable from the outside, but once it clicks, you see it everywhere and it makes perfect sense.

This guide is for complete beginners.

I’m going to walk you through what ex-dividend means, why it matters so much for anyone hoping to build a second income from shares, and how you can use this knowledge to make smarter decisions – all without drowning you in City jargon.

We’ll cover everything from FTSE 100 dividend shares to the clever ways you can shelter your dividends inside an ISA or SIPP. Relax, and let’s get started.

But here’s the truth... once you’ve spent ten minutes with the idea, you’ll wonder what all the fuss was about.

Understanding the ex-dividend date is a bit like learning the offside rule in football. It feels impenetrable from the outside, but once it clicks, you see it everywhere and it makes perfect sense.

This guide is for complete beginners.

I’m going to walk you through what ex-dividend means, why it matters so much for anyone hoping to build a second income from shares, and how you can use this knowledge to make smarter decisions – all without drowning you in City jargon.

We’ll cover everything from FTSE 100 dividend shares to the clever ways you can shelter your dividends inside an ISA or SIPP. Relax, and let’s get started.

What Does Ex-Dividend Actually Mean? The Bakery Analogy

Imagine you run a much-loved local bakery. Business is good, so you decide to share some of the profits with your regulars by giving away a free sourdough loaf to every registered member of your loyalty scheme. But you can’t hand out bread to the entire neighbourhood... you need a cut-off point. You announce that only people who are on the membership list by 5p.m. on Friday will get the free loaf the following Monday. If someone signs up on Saturday morning, I’m afraid they’ve missed the boat. They’ll have to wait for the next giveaway.

In the world of shares, that Friday 5p.m. deadline is the record date. The point just before it – the moment when new buyers no longer qualify for the upcoming dividend – is the ex-dividend date.

When a share goes ex-dividend, anyone buying from that moment onwards does not receive the next dividend payment. The dividend stays with the seller.

So, the ex-dividend date is simply the first day on which a share trades without the right to the next dividend.

If you already own the shares on the day before the ex-dividend date, you’ll get the dividend. If you buy on the ex-dividend date itself, you won’t. Simple as that.

Before a share reaches its ex-dividend date, it’s said to be trading cum dividend – literally ‘with dividend’.

You’ll see that Latin phrase crop up in old-school broker reports, but all you need to remember is that cum dividend means the dividend is attached.

Once the ex-dividend date arrives, the share price adjusts to reflect the fact that the buyer no longer gets the payout.

The term ex-dividend appears on almost every dividend calendar you’ll ever look at, and I encourage you to embrace it rather than fear it.

When I was still finding my feet, I’d circle ex-dividend dates in a paper diary – I still keep a digital version today. Knowing these dates gives you control over exactly when you receive your income.

If someone signs up on Saturday morning, I’m afraid they’ve missed the boat. They’ll have to wait for the next giveaway.

In the world of shares, that Friday 5p.m. deadline is the record date. The point just before it – the moment when new buyers no longer qualify for the upcoming dividend – is the ex-dividend date.

When a share goes ex-dividend, anyone buying from that moment onwards does not receive the next dividend payment. The dividend stays with the seller.

So, the ex-dividend date is simply the first day on which a share trades without the right to the next dividend.

If you already own the shares on the day before the ex-dividend date, you’ll get the dividend. If you buy on the ex-dividend date itself, you won’t. Simple as that.

Before a share reaches its ex-dividend date, it’s said to be trading cum dividend – literally ‘with dividend’.

You’ll see that Latin phrase crop up in old-school broker reports, but all you need to remember is that cum dividend means the dividend is attached.

Once the ex-dividend date arrives, the share price adjusts to reflect the fact that the buyer no longer gets the payout.

The term ex-dividend appears on almost every dividend calendar you’ll ever look at, and I encourage you to embrace it rather than fear it.

When I was still finding my feet, I’d circle ex-dividend dates in a paper diary – I still keep a digital version today. Knowing these dates gives you control over exactly when you receive your income.

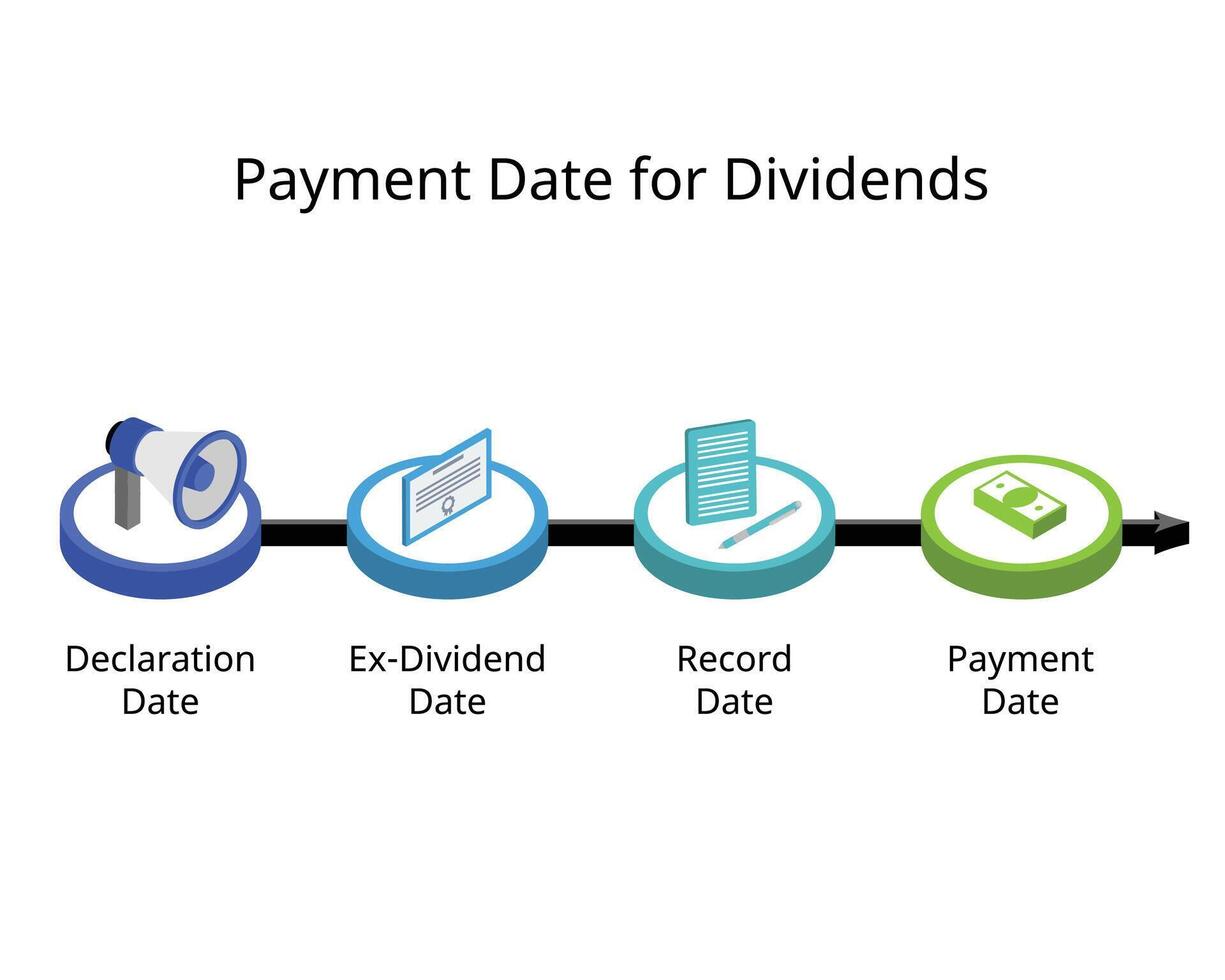

The Lifecycle of A Dividend:

Key Dates Every Investor Should Know

Declaration Date: The Announcement

Everything starts when a company publishes its financial results. The board of directors will propose a dividend and announce the key dates that follow. This is called the declaration date. You might read something like: “The board has declared an interim dividend of 25p per share.” Alongside that headline figure, the company will publish the ex-dividend date, the record date, and the payment date. I always check the declaration notice on the company’s investor relations page – it’s the source of truth. Write those dates down. Trust me, a missed ex-dividend date because you didn’t note it down can feel like finding a gift voucher at the back of a drawer and discovering it expired yesterday.Cum-Dividend Period: The Qualifying Window

From the declaration date right up until the day before the ex-dividend date, the shares are in their cum dividend phase. If you buy during this window, you will be entitled to the declared dividend. Many new investors don’t realise that they can buy just one day before the ex-dividend date and still qualify. You don’t need to have held the shares for months... ownership on that one crucial day is enough. I’ve done this myself on plenty of occasions – I spotted a high-quality FTSE 100 dividend share I wanted for the long term, bought it the day before it went ex-dividend, and collected the payout a few weeks later. That felt like a big win.Ex-Dividend Date: The Cut-Off Point

And now the star of our show. The ex-dividend date is the day the shares begin trading without the right to the dividend. In the UK, the ex-dividend date is typically one business day before the record date. If you place a buy order on the morning of the ex-dividend date, the trade will settle after the record date, meaning you won’t appear on the shareholder register in time. The dividend belongs to the seller. Knowing this is fundamental for anyone serious about making money from the stock market through dividends.Record Date: The Official Snapshot

The record date is when the company closes its shareholder register and takes a snapshot. Every person on that list gets the dividend. Because UK shares settle on a T+2 basis (trade date plus two business days), you need to have bought at least one day before the ex-dividend date to be on the register by the record date. I’ve seen beginners panic when they misunderstand the timeline, thinking the record date is the deadline. It isn’t... the ex-dividend date is the real cut-off for you as a buyer.Payment Date: Cash In Your Pocket

Finally, the payment date arrives. The company sends the dividend directly to your brokerage account or your bank account. If you hold shares inside an ISA or SIPP, the cash stays in that tax-efficient wrapper. For me, payment dates are like birthday mornings dotted throughout the year. I use them to reinvest or just admire the growing snowball of passive income.

Why The Ex-Dividend Date Matters For Your Income

I meet a lot of people who say, “I want to live off dividends one day.” That’s a wonderful goal – it’s one I share – but it only works if you understand the rhythm of dividend payments. The ex-dividend date is the drumbeat. When you’re building a portfolio of income-producing shares, you’re not just picking companies at random. You’re choreographing a stream of cash flows. If you want, say, £3,000 a month in dividend income, you need to know which companies are paying out and when. You need to know when each share goes ex-dividend so you can predict when the money will land. I learned this lesson the hard way early in my journey. I’d bought a stake in a well-known British utility company and was expecting a huge dividend in December.

I’d completely misread the ex-dividend date – I’d bought the shares three days after it. December came and went, and no dividend arrived.

I was disappointed, but I had nobody to blame except myself. That blunder taught me to treat the ex-dividend calendar with almost religious devotion.

Knowing the ex-dividend schedule also lets you plan for tax efficiency. Outside an ISA, UK dividend income above your annual allowance is taxable.

But if you plan your purchases around ex-dividend dates and keep your income-generating assets inside an ISA or SIPP, you never need to share a penny of that hard-earned dividend with HMRC.

I learned this lesson the hard way early in my journey. I’d bought a stake in a well-known British utility company and was expecting a huge dividend in December.

I’d completely misread the ex-dividend date – I’d bought the shares three days after it. December came and went, and no dividend arrived.

I was disappointed, but I had nobody to blame except myself. That blunder taught me to treat the ex-dividend calendar with almost religious devotion.

Knowing the ex-dividend schedule also lets you plan for tax efficiency. Outside an ISA, UK dividend income above your annual allowance is taxable.

But if you plan your purchases around ex-dividend dates and keep your income-generating assets inside an ISA or SIPP, you never need to share a penny of that hard-earned dividend with HMRC.

How The Share Price Reacts On The Ex-Dividend Date:

The Basket of Apples

When a share goes ex-dividend, its price is theoretically reduced by the amount of the dividend.

If a FTSE 100 dividend share closed at 500p (£5) the night before the ex-dividend date and the dividend is 50p, the market will typically open the share at around 450p (£4.50), all else being equal.

In the real world, other market forces move the price as well, so you might not see a perfect 50p drop.

But the principle holds... the dividend comes out of the share price.

This is crucial because it means you haven’t found a magic loophole. You can’t just buy a share the day before it goes ex-dividend, pocket the dividend, and sell the next day for the same price. The market adjusts.

I’ve seen a few investors try what’s known as a dividend capture strategy – buying just before the ex-dividend date and selling shortly after, aiming to bag the payout without holding the shares for long.

On paper, it looks tempting. In practice, the share price drop often erases the gain, and trading costs plus the bid-offer spread can add up in fees.

A dividend capture strategy isn’t a substitute for owning wonderful companies for the long haul. I’ve tried it once or twice in my younger days... the numbers never quite added up the way I’d imagined.

That said, the share price adjustment isn’t a reason to fear the ex-dividend date. If you’re a genuine long-term income investor, the price drop is temporary.

Quality companies grow their earnings and dividends over time, and the share price recovers. You simply collect your dividends and wait.

When a share goes ex-dividend, its price is theoretically reduced by the amount of the dividend.

If a FTSE 100 dividend share closed at 500p (£5) the night before the ex-dividend date and the dividend is 50p, the market will typically open the share at around 450p (£4.50), all else being equal.

In the real world, other market forces move the price as well, so you might not see a perfect 50p drop.

But the principle holds... the dividend comes out of the share price.

This is crucial because it means you haven’t found a magic loophole. You can’t just buy a share the day before it goes ex-dividend, pocket the dividend, and sell the next day for the same price. The market adjusts.

I’ve seen a few investors try what’s known as a dividend capture strategy – buying just before the ex-dividend date and selling shortly after, aiming to bag the payout without holding the shares for long.

On paper, it looks tempting. In practice, the share price drop often erases the gain, and trading costs plus the bid-offer spread can add up in fees.

A dividend capture strategy isn’t a substitute for owning wonderful companies for the long haul. I’ve tried it once or twice in my younger days... the numbers never quite added up the way I’d imagined.

That said, the share price adjustment isn’t a reason to fear the ex-dividend date. If you’re a genuine long-term income investor, the price drop is temporary.

Quality companies grow their earnings and dividends over time, and the share price recovers. You simply collect your dividends and wait.

The Settlement Rule: Why T+2 Is Your Friend (And Foe)

In the UK, standard share trades settle two business days after the trade date – that’s the T+2 rule. This little piece of plumbing explains why the ex-dividend date sits one business day before the record date. Think of it as a two-day conveyor belt. If you want to be on the shareholder register by the record date, your trade must have settled by then. To settle by the record date, you have to buy at least two business days earlier. That means the last day you can buy and still catch the settlement deadline is the day before the ex-dividend date. Let me make it concrete... ...Suppose a company sets its record date on a Thursday. Working backwards two business days gives you Tuesday as the last day to trade and settle by Thursday. That makes Wednesday the ex-dividend date. Buy on Wednesday, and your trade settles on Friday – too late for the Thursday record date. So you miss the dividend. I always tell my coaching clients who are new to dividend investing to ignore the record date for their purchase decision. Focus entirely on the ex-dividend date. Own the shares before that day, and you’re golden. Buy on the ex-dividend date, and you’re waiting another three, six, or twelve months for the next payout.Ex-Dividend And Tax-Efficient Accounts:

Using ISAs And SIPPs Wisely

The same goes for a SIPP, though the tax treatment is slightly different because you get tax relief on contributions and pay income tax when you withdraw.

The point is, the dividends themselves grow without the taxman taking a slice.

Now, here’s where the ex-dividend date plays a starring role. The UK tax year runs from 6 April to 5 April. If you’re holding dividend-paying shares outside an ISA – in a general investment account – you have an annual dividend allowance.

Dividend income above that allowance is taxable at your marginal rate. Knowing exactly when your shares go ex-dividend lets you anticipate when the cash will arrive and within which tax year it will fall.

A big dividend that lands on 3 April is taxed in one year... the same dividend arriving on 8 April falls into the next tax year, giving you a fresh allowance to use.

But my strongest advice to you is this... fill your ISA allowance first. When you buy a FTSE 100 dividend share inside an ISA and it goes ex-dividend, the resulting payment stays sheltered forever.

You can reinvest it, spend it, or keep it as cash – no tax return required. It’s one of the greatest gifts the UK government gives to ordinary investors.

SIPPs work similarly for those building a retirement pot. If you’re still working and decades from retirement, holding dividend shares in a SIPP means you’re turbocharging your pension with tax-relieved contributions and tax-free dividend growth.

Ex-dividend dates don’t directly change the SIPP wrapper, but knowing when your dividends land helps you decide when to reinvest, rebalance, or simply admire your progress.

The same goes for a SIPP, though the tax treatment is slightly different because you get tax relief on contributions and pay income tax when you withdraw.

The point is, the dividends themselves grow without the taxman taking a slice.

Now, here’s where the ex-dividend date plays a starring role. The UK tax year runs from 6 April to 5 April. If you’re holding dividend-paying shares outside an ISA – in a general investment account – you have an annual dividend allowance.

Dividend income above that allowance is taxable at your marginal rate. Knowing exactly when your shares go ex-dividend lets you anticipate when the cash will arrive and within which tax year it will fall.

A big dividend that lands on 3 April is taxed in one year... the same dividend arriving on 8 April falls into the next tax year, giving you a fresh allowance to use.

But my strongest advice to you is this... fill your ISA allowance first. When you buy a FTSE 100 dividend share inside an ISA and it goes ex-dividend, the resulting payment stays sheltered forever.

You can reinvest it, spend it, or keep it as cash – no tax return required. It’s one of the greatest gifts the UK government gives to ordinary investors.

SIPPs work similarly for those building a retirement pot. If you’re still working and decades from retirement, holding dividend shares in a SIPP means you’re turbocharging your pension with tax-relieved contributions and tax-free dividend growth.

Ex-dividend dates don’t directly change the SIPP wrapper, but knowing when your dividends land helps you decide when to reinvest, rebalance, or simply admire your progress.

Common Blunder Beginners Make Around Ex-Dividend Dates

Over the years, I’ve mentored a handful of friends who wanted to start dividend investing, and I’ve watched them trip over the same hurdles. Let me share the most frequent blunders so you can step right over them. Blunder 1: Thinking the record date is the deadline. I’ve said it before, but it bears repeating. The record date is an administrative date for the company, not your shopping deadline. The ex-dividend date is the cut-off that matters. Always check the ex-dividend date before buying. Blunder 2: Ignoring the share price drop and feeling deceived. I once had a colleague phone me in a panic: “The share price fell exactly by the dividend amount! Something’s not right!” Everything was ok. The market was simply reflecting that the dividend was no longer attached. If you’re a long-term holder, the price will fluctuate around many events. Don’t let the ex-dividend price adjustment spook you out of a quality company. Blunder 3: Chasing high dividend yields without checking the ex-dividend timeline. A high dividend yield can be a warning sign. Sometimes a share price has slumped because the market expects the dividend to be cut. I once bought into a company with a 9% yield just before its ex-dividend date, feeling very clever. The dividend was indeed paid, but soon after the company slashed its payout, and the share price fell further. The ex-dividend date doesn’t protect you from dodgy business fundamentals. Blunder 4: Trying a dividend capture strategy without understanding costs. As I mentioned earlier, the idea of jumping in and out around ex-dividend dates sounds appealing. But stamp duty, broker fees, and the bid-offer spread are real costs. I’ve crunched the numbers countless times, and for a retail investor, a dividend capture approach rarely delivers reliable profits after costs. I’d rather hold a great business and collect dividends year after year. Blunder 5: Not checking if the company pays in a foreign currency. Several popular dividend shares listed on the London Stock Exchange actually declare dividends in euros or US dollars. The ex-dividend date is still published in UK terms, but the payment amount can fluctuate with exchange rates. I hold shares in a couple of US/European giants, and I always note the ex-dividend date and the currency exposure, so I’m not surprised when the sterling amount varies. Blunder 6: Forgetting to reinvest dividends automatically. Once you know your shares have gone ex-dividend and the cash is on its way, you have a choice. You can let the money sit as cash, or you can reinvest it. Many platforms offer dividend reinvestment plans that automatically buy more shares for you. By ignoring this, you miss out on compounding. I’ve set my ISA to reinvest dividends from several holdings – it’s like a self-watering plant.Building A Dividend Calendar Around Ex-Dividend Dates

If you’re serious about making money from the stock market through dividends, you need a calendar. I don’t mean a flimsy wall chart... I mean a simple digital spreadsheet or a dedicated note on your phone that lists the ex-dividend dates for every share you own or want to own.

Here’s how I do it. I maintain a simple table with four columns: company name, ex-dividend date, payment date, and dividend amount per share.

Every time a company makes a declaration, I update the row. At a glance, I can see that some companies normally goes ex-dividend in late December and pays in February, or that other company’s quarterly cycle means ex-dividend dates in February, May, August, and November.

I’ve even colour-coded months to visualise my monthly income flow.

This exercise brings the ex-dividend concept to life. You start to see the rhythm of your portfolio. You can spot gaps – perhaps you receive very little in April, so you might look for a quality share that goes ex-dividend in March to plug that gap.

You begin to think like an income farmer, planting seeds before the ex-dividend window closes and harvesting cash weeks later.

Free resources can help. Most financial websites publish ex-dividend calendars for the FTSE 100, FTSE 250, and beyond.

A quick search for “FTSE 100 dividend dates” will give you a list of upcoming ex-dividend dates.

I don’t mean a flimsy wall chart... I mean a simple digital spreadsheet or a dedicated note on your phone that lists the ex-dividend dates for every share you own or want to own.

Here’s how I do it. I maintain a simple table with four columns: company name, ex-dividend date, payment date, and dividend amount per share.

Every time a company makes a declaration, I update the row. At a glance, I can see that some companies normally goes ex-dividend in late December and pays in February, or that other company’s quarterly cycle means ex-dividend dates in February, May, August, and November.

I’ve even colour-coded months to visualise my monthly income flow.

This exercise brings the ex-dividend concept to life. You start to see the rhythm of your portfolio. You can spot gaps – perhaps you receive very little in April, so you might look for a quality share that goes ex-dividend in March to plug that gap.

You begin to think like an income farmer, planting seeds before the ex-dividend window closes and harvesting cash weeks later.

Free resources can help. Most financial websites publish ex-dividend calendars for the FTSE 100, FTSE 250, and beyond.

A quick search for “FTSE 100 dividend dates” will give you a list of upcoming ex-dividend dates.

Real-World Example: A FTSE 100 Giant Goes Ex-Dividend

Let’s put some flesh on the bones with a concrete example. Imagine a well-known UK-listed company – let’s call it “Cheshire Holdings plc”. Cheshire Holdings has a long track record of paying reliable dividends. In late July, the board declares a third-quarter dividend of 25p per share. In the announcement, they state...- Ex-dividend date: Thursday, 10 August

- Record date: Friday, 11 August

- Payment date: Monday, 11 September

Why Focusing On The Ex-Dividend Date Makes You A Better Investor

I’ve noticed that investors who ignore ex-dividend dates tend to view dividends as a vague, occasional bonus – a bit like finding a fiver in an old coat. Investors who pay attention to ex-dividend dates see dividends as a predictable income stream they can shape and depend on. That shift in mindset is enormous. When you know exactly when your shares will go ex-dividend, you can plan your bills, your holidays, and your reinvestment strategy with confidence. You stop chasing hot tips and start building a portfolio that pays you on a schedule you understand. This sense of control is what separates successful dividend investors from perpetual speculators. I’ll share a small personal story. A few years ago, I decided I wanted my portfolio to pay me a meaningful sum every quarter to cover my family’s utility bills. I listed our typical quarterly energy bill and then worked backwards: I needed certain dividend-paying shares with ex-dividend dates falling roughly one to two months before each bill was due, so the cash would arrive in time. I reshuffled a few holdings, added a couple of investment trusts, and within eighteen months I’d built a mini income engine that spat out cash precisely when I needed it. That wouldn’t have been possible without understanding the ex-dividend mechanic. It felt like financial brilliance, but it was really just careful date-matching.Ex-Dividend And Your Investment Strategy:

Long-Term Income vs Short-Term Tricks

How To Find Ex-Dividend Dates For UK Shares

This is the practical bit. You don’t need an expensive data terminal. Here are my favourite ways to find ex-dividend dates...- Company investor relations websites. Go straight to the source. Look for “financial calendar” or “dividend information.” You’ll find declaration dates, ex-dividend dates, record dates, and payment dates all clearly set out.

- London Stock Exchange website. The LSE has a dividend calendar that shows upcoming ex-dividend dates for listed companies. It’s free and updated regularly.

- Broker platforms. Most of the major UK investment platforms now display upcoming ex-dividend dates in your portfolio view. I use this feature to quickly scan which of my holdings will go ex-dividend in the coming fortnight.

- Financial news sites. Websites like Hargreaves Lansdown, AJ Bell, and Interactive Investor publish dividend calendars. Even a general search for “UK dividend dates this week” will bring up useful tables.

- Dedicated dividend newsletters. Some investors I know subscribe to free email newsletters that summarise ex-dividend dates for the week ahead. It’s a handy prompt.

Ex-Dividend Dates And Market Emotions:

Staying Calm Amid The Noise

Frequently Asked Questions About Ex-Dividend Dates

What exactly is the ex-dividend date?

The ex-dividend date is the first day on which a share trades without the right to the next dividend payment. If you buy shares on or after this date, you will not receive the upcoming dividend — it stays with the seller. If you already own the shares the day before the ex-dividend date, you will get the dividend.

Do I need to own shares for a long time to qualify for the dividend?

No. Many new investors don't realise they can buy just one day before the ex-dividend date and still qualify. You don't need to have held the shares for months; ownership on that one crucial day is enough.

What is the record date, and why shouldn't I treat it as my deadline?

The record date is when the company closes its shareholder register and takes a snapshot to see who gets the dividend. However, because UK shares settle on a T+2 basis (trade date plus two business days), you need to buy at least one day before the ex-dividend date to be on the register by the record date. The ex-dividend date is the real cut-off for you as a buyer — the record date is just an administrative date for the company.

Why does the share price often drop on the ex-dividend date?

When a share goes ex-dividend, its price is theoretically reduced by the amount of the dividend. This is a mechanical market adjustment, not a sign of panic or bad news. For example, if a share closed at 500p and the dividend is 50p, the market will typically open it at around 450p. The dividend comes out of the share price — it's not a loophole you can exploit.

What does "cum dividend" mean?

"Cum dividend" is a Latin phrase meaning "with dividend". The period from the declaration date right up until the day before the ex-dividend date is the cum-dividend phase. If you buy during this window, you will be entitled to the declared dividend.

What are the four key dates in the dividend timeline?

The four key dates are:

- Declaration Date — The company announces the dividend and publishes the key dates that follow.

- Ex-Dividend Date — The cut-off day when shares start trading without the dividend right.

- Record Date — The company takes a snapshot of its shareholder register.

- Payment Date — The company sends the dividend to your brokerage or bank account.

How does holding dividend shares in an ISA or SIPP help with tax?

Inside a Stocks and Shares ISA, every dividend you receive is completely tax-free. The same goes for a SIPP, where dividends grow without the taxman taking a slice. My strongest advice is to fill your ISA allowance first — when you buy a FTSE 100 dividend share inside an ISA and it goes ex-dividend, the payment stays sheltered forever, with no tax return required.

Is the "dividend capture strategy" a good idea?

A dividend capture strategy — buying just before the ex-dividend date and selling shortly after to bag the payout — is usually not a reliable long-term plan. In practice, the share price drop often erases the gain, and trading costs plus the bid-offer spread add up in fees. For a retail investor, this approach rarely delivers reliable profits after costs. It's better to hold great businesses and collect dividends year after year.

How can I track upcoming ex-dividend dates?

You can find ex-dividend dates through several free resources:

- Company investor relations websites — look for "financial calendar" or "dividend information".

- London Stock Exchange website — has a free, updated dividend calendar.

- Broker platforms — most major UK platforms display upcoming ex-dividend dates in your portfolio view.

- Financial news sites — like Hargreaves Lansdown, AJ Bell, and Interactive Investor.

- Dividend newsletters — free email summaries of the week ahead.

I recommend maintaining a simple spreadsheet with four columns: company name, ex-dividend date, payment date, and dividend amount per share.

Should I worry when a share price drops on the ex-dividend date?

No. The drop is largely synthetic — an accounting adjustment, not a verdict on the company. I mentally tag every ex-dividend date as a "known event" and expect a price dip. If the dip is roughly equal to the dividend, everything is normal. Staying calm around ex-dividend dates has saved me from countless poor decisions, and I've often used the post-ex-dividend dip to add more shares at a slightly lower price.

Key Takeaways

Let’s wrap up with a clear, summary of what you need to remember about ex-dividend dates and how to use them to your advantage.| 💡 Key Takeaways |

|---|

| The ex-dividend date is the day a share starts trading without the right to the next dividend. If you buy on or after this date, you won't get the upcoming payout. |

| To qualify for a dividend, you must own the shares before the ex-dividend date. The record date is an administrative cut-off; your practical deadline is the day before the ex-dividend date, due to the T+2 settlement rule. |

| Shares typically fall in price by the amount of the dividend on the ex-dividend date. This is a mechanical market adjustment, not a sign of an issue. |

| The period before the ex-dividend date is called the cum dividend period. Buying during this window ensures you receive the declared dividend. |

| Key dates in the dividend timeline are the declaration date, ex-dividend date, record date, and payment date. Familiarise yourself with all four to master your income planning. |

| Holding dividend shares inside an ISA or SIPP shelters your dividend income from tax. The ex-dividend date remains the same, but the tax treatment is far more favourable. |

| A dividend capture strategy (buying just before the ex-dividend date and selling after) is usually not a reliable long-term plan due to price adjustment, trading costs, and taxes. |

| Regularly tracking ex-dividend dates helps you predict cash flow, reinvest dividends, and avoid the frustration of missing a payout. |

| FTSE 100 dividend shares often have well-established dividend calendars. Use free online calendars to stay informed, and record the dates in your own spreadsheet. |

| A calm, long-term approach to ex-dividend dates transforms dividend investing from a guessing game into a predictable, dependable income strategy. |