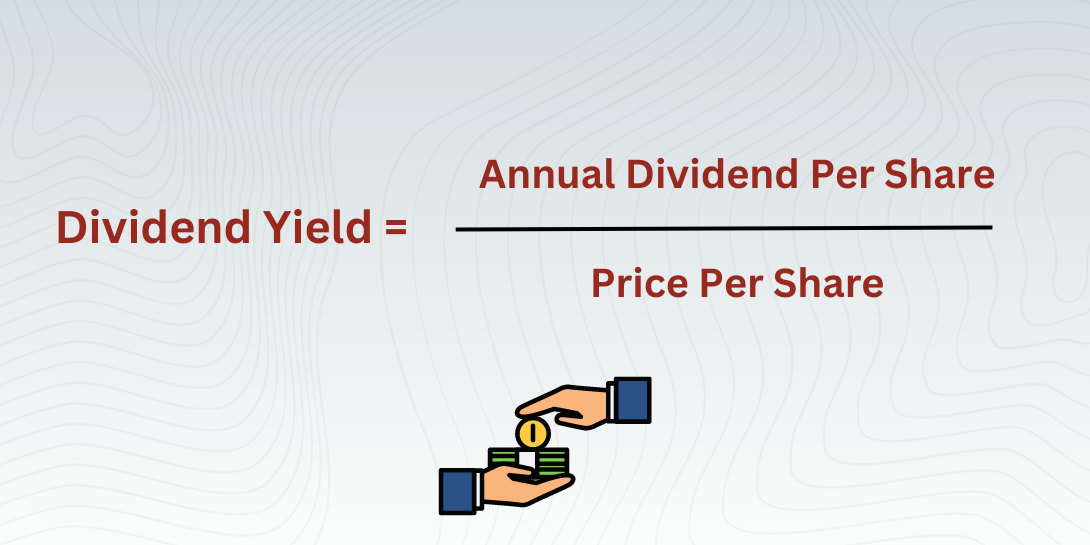

Dividend Yield:

The Simple Secret To My

Early Retirement At 23

I want to take you by the hand and demystify dividend yield. No jargon, no complicated formulas that make your eyes glaze over.

Just a warm, honest advice about how this single percentage can transform your relationship with money.

If you’re looking for dividend investing for beginners, this is your foundation.

Once you grasp dividend yield, everything else in the income-investing world starts to click.

And the best part? You can start building your own stream of stock market income with as little as £25 a month.

Let me show you how.

I want to take you by the hand and demystify dividend yield. No jargon, no complicated formulas that make your eyes glaze over.

Just a warm, honest advice about how this single percentage can transform your relationship with money.

If you’re looking for dividend investing for beginners, this is your foundation.

Once you grasp dividend yield, everything else in the income-investing world starts to click.

And the best part? You can start building your own stream of stock market income with as little as £25 a month.

Let me show you how.

What Exactly Is Dividend Yield? (Breathe – It’s Simpler Than You Think)

Before we label it with the term dividend yield, let’s strip everything back. Imagine you own a corner shop. Every year, after all the stuff, staff wages, and electricity bills have been paid, the shop generates a profit. As the owner, you take a portion of that profit and put it into your personal bank account. That’s a dividend. Now, if a friend asked you, “How good is that shop at putting cash in your pocket compared to what you paid for it?”, you’d naturally compare the annual cash you pocketed to the price you originally paid to buy the shop. If you paid £100,000 for the shop and it handed you £5,000 in dividends each year, you’d say you’re earning 5% on your money. That 5% is, in essence, the dividend yield. Bringing this into the stock market, a company’s dividend yield tells you how much income you’re getting for every pound you invest in its shares. It’s the annual dividend per share divided by the share price, expressed as a percentage. So if a company pays out 10p per share over the course of a year, and one share currently costs £2.00 (200p), the dividend yield is 5% (10p divided by 200p, multiplied by 100). That’s it. You now know what hundreds of books try to make sound intimidating.

The Rental Property Analogy That Also Makes Dividend Yield Crystal Clear

Another good analogy that made dividend yield stick for me – and the one I still use to explain to my coaching clients – is buy-to-let property. Picture this... you buy a terraced house in Sheffield for £180,000. You don’t live in it... you rent it out. Every month your tenant pays you £925, which after a few minor expenses leaves you with a net income of £800 a month. Over a year, that’s £9,600 of pure income. If we could invest in property on the stock market, we’d say the dividend yield of that house is £9,600 divided by £180,000, which equals 5.3%.

Now, everything you instinctively understand about property applies beautifully to dividend yield investing.

You wouldn’t buy a house just because the tenant promised an enormous rent for one year, would you?

You’d look at the neighbourhood, the condition of the roof, and whether that rent is sustainable long term.

You’d want a reliable tenant who doesn’t trash the place and who pays consistently.

In the world of dividend yield, the tenant is the company’s profit, the rent is the dividend, and the roof is the balance sheet.

If someone offered you a 12% rental yield on a property, your alarm bells would ring.

You'd be suspicious. The same suspicion should accompany any seductively high dividend yield.

A yield that looks too good to be true often is – a company might be in distress, with a share price that’s cratered, making the historical dividend look artificially inflated.

That’s how novice income seekers get trapped. But when you find a solid, boring company with a reasonable, growing dividend yield, you’ve essentially acquired a well-built rental property with long-term tenants.

And that, my friend, is the game.

Over a year, that’s £9,600 of pure income. If we could invest in property on the stock market, we’d say the dividend yield of that house is £9,600 divided by £180,000, which equals 5.3%.

Now, everything you instinctively understand about property applies beautifully to dividend yield investing.

You wouldn’t buy a house just because the tenant promised an enormous rent for one year, would you?

You’d look at the neighbourhood, the condition of the roof, and whether that rent is sustainable long term.

You’d want a reliable tenant who doesn’t trash the place and who pays consistently.

In the world of dividend yield, the tenant is the company’s profit, the rent is the dividend, and the roof is the balance sheet.

If someone offered you a 12% rental yield on a property, your alarm bells would ring.

You'd be suspicious. The same suspicion should accompany any seductively high dividend yield.

A yield that looks too good to be true often is – a company might be in distress, with a share price that’s cratered, making the historical dividend look artificially inflated.

That’s how novice income seekers get trapped. But when you find a solid, boring company with a reasonable, growing dividend yield, you’ve essentially acquired a well-built rental property with long-term tenants.

And that, my friend, is the game.

How To Calculate Dividend Yield Without Feeling Like You’re Back At School

You can leave the calculator in the drawer. Calculating dividend yield takes about thirty seconds once you know where to look. The formula is simply... Dividend Yield = (Annual Dividend Per Share ÷ Current Share Price) × 100 The “annual dividend per share” is the total amount of dividends a company has declared it will pay over the coming year.

Why Dividend Yield Matters So Deeply For Passive Income From Shares

You’ve probably dreamt about waking up to find money has magically appeared in your account. That’s exactly what passive income from shares feels like, and dividend yield is the engine. When you focus on dividend yield, you’re not hoping for a quick-flip share price surge that may never arrive.

You’re methodically building a machine that churns out cash four, eight, twelve times a year across all the companies you own.

What hooked me as an 18-year-old with a bulky second-hand laptop wasn’t capital gains.

It was the predictability of those little “dividend received” notifications.

Every time a dividend landed, my portfolio’s dividend yield – when calculated against the original capital I’d invested – edged up relative to what I had put in.

This is what experienced investors call “yield on cost”. If I bought shares at £1.00 with a 10p dividend, my initial dividend yield was 10%.

Five years later, if that dividend had grown to 14p, my yield on original cost was 14%, even if the share price had doubled and the current yield to new investors was only 7%.

This is the magic that early adopters feel... your money starts working harder than you do.

And the real gift? Dividends don’t ask for your permission. You don’t need to ring up the company and request payment.

As long as you own the shares before the ex-dividend date (the date by which you must be on the shareholder register), the cash simply appears in your brokerage account.

You can then spend it on bills, reinvest it, or use it to buy yourself a little something while the underlying shares quietly keep generating tomorrow’s income.

This is the psychological freedom that understanding dividend yield gave me – a freedom far bigger than early retirement itself.

When you focus on dividend yield, you’re not hoping for a quick-flip share price surge that may never arrive.

You’re methodically building a machine that churns out cash four, eight, twelve times a year across all the companies you own.

What hooked me as an 18-year-old with a bulky second-hand laptop wasn’t capital gains.

It was the predictability of those little “dividend received” notifications.

Every time a dividend landed, my portfolio’s dividend yield – when calculated against the original capital I’d invested – edged up relative to what I had put in.

This is what experienced investors call “yield on cost”. If I bought shares at £1.00 with a 10p dividend, my initial dividend yield was 10%.

Five years later, if that dividend had grown to 14p, my yield on original cost was 14%, even if the share price had doubled and the current yield to new investors was only 7%.

This is the magic that early adopters feel... your money starts working harder than you do.

And the real gift? Dividends don’t ask for your permission. You don’t need to ring up the company and request payment.

As long as you own the shares before the ex-dividend date (the date by which you must be on the shareholder register), the cash simply appears in your brokerage account.

You can then spend it on bills, reinvest it, or use it to buy yourself a little something while the underlying shares quietly keep generating tomorrow’s income.

This is the psychological freedom that understanding dividend yield gave me – a freedom far bigger than early retirement itself.

The Danger of Chasing High Dividend Yield Stocks (Please Read This Section Carefully)

Now we get to the bit that separates successful income investors from the casualties. A sky-high dividend yield can feel like a siren call. I’ve watched people pile into stocks offering 10%, 15%, even 20% yields, convinced they’d cracked the code. Most got burned. Here’s an example I want you to understand... Trendy Street Retail PLC (again its a made up company) has its share price fallen from £5.00 to £1.00 because high street footfall is vanishing and profits are evaporating. The company hasn’t yet cut its dividend... it’s still paying an annual 20p per share. The dividend yield now screams 20%. A beginner spots this and thinks, “Blimey, 20%! I’ll have some of that.” They pour money in, only for Trendy Street Retail to announce three months later that the dividend is being suspended entirely because the company is haemorrhaging cash. The share price falls further to 40p, and our investor friend is left holding a 60% capital loss with zero income. The yield vanished like morning mist. This is the classic “dividend yield trap”. The trap exists because dividend yield is a simple ratio with two moving parts. If the share price plummets faster than the dividend is reduced, the yield spikes, luring the unwary. A genuinely safe, growing dividend yield usually sits somewhere in the 2%–4.5% range for most healthy UK dividend stocks. Some sectors, like certain renewable infrastructure funds, might offer a reliable 6%–8%, but you must understand why the yield is elevated before buying. Is it a temporary market overreaction to a non-fatal issue (opportunity), or is the business itself in structural decline (danger)? This is precisely why I ignore any dividend yield above 7% until I’ve done at least an afternoon of homework. I check whether the dividend is covered by earnings, whether debt is manageable, and whether the company’s competitive position is intact. Which brings us to the single most important safety check you’ll ever learn.The Dividend Payout Ratio: The Safety Net Behind Every Dividend Yield

You wouldn’t rent a flat without checking the gas safety certificate. So please don’t buy a share for its dividend yield without glancing at the dividend payout ratio. It’s the financial equivalent of that safety check. The dividend payout ratio tells you what percentage of a company’s profits are being paid out as dividends. If a company earns £100 million in profit and pays out £60 million in dividends, the payout ratio is 60%. That feels comfortable. The company retains the remaining £40 million to reinvest in growth, pay down debt, or build a rainy-day fund.

If profits dip next year, there’s a buffer before the dividend needs to be cut.

But when you see a dividend yield that’s deliciously high, often the payout ratio has ballooned well above 100%.

That means the company is paying out more in dividends than it actually earns.

It’s paying you out of borrowed money, asset sales, or accumulated reserves. That can’t last forever.

Eventually, the board will slash the dividend, the yield will collapse, and the share price will likely tumble too.

I generally look for a payout ratio of 60% and below for most mature UK dividend payers.

If the ratio is below 60%, the company might be able to grow its dividend faster than the share price appreciates, gradually increasing the dividend yield on my original investment.

If it’s above 80%, I’m cautious. Above 100% and I’m usually walking away unless there’s an exceptional, temporary reason.

A steady dividend payout ratio is the silent protector of your income.

It’s not complicated – anyone can find it on a free financial website – yet most yield-chasers never look at it.

You will now, and that simple habit puts you streets ahead.

The company retains the remaining £40 million to reinvest in growth, pay down debt, or build a rainy-day fund.

If profits dip next year, there’s a buffer before the dividend needs to be cut.

But when you see a dividend yield that’s deliciously high, often the payout ratio has ballooned well above 100%.

That means the company is paying out more in dividends than it actually earns.

It’s paying you out of borrowed money, asset sales, or accumulated reserves. That can’t last forever.

Eventually, the board will slash the dividend, the yield will collapse, and the share price will likely tumble too.

I generally look for a payout ratio of 60% and below for most mature UK dividend payers.

If the ratio is below 60%, the company might be able to grow its dividend faster than the share price appreciates, gradually increasing the dividend yield on my original investment.

If it’s above 80%, I’m cautious. Above 100% and I’m usually walking away unless there’s an exceptional, temporary reason.

A steady dividend payout ratio is the silent protector of your income.

It’s not complicated – anyone can find it on a free financial website – yet most yield-chasers never look at it.

You will now, and that simple habit puts you streets ahead.

How to Start Your Dividend Investing Journey (Even With £25 A Month)

The most common phrase I hear is “I don’t have enough money to start investing.” I promise you, I started with spare cash from various odd jobs. What matters isn’t the lump sum... it’s the system. The first step is opening a Stocks and Shares ISA. Here in the UK, an ISA shelters all your dividends and capital gains from the taxman. Every pound of dividend yield you generate inside an ISA is yours to keep, completely tax-free. This is the bedrock of ISA dividend investing, and I wouldn’t dream of starting anywhere else. The current ISA allowance is £20,000 per year, far more than most beginners need, which means you can grow an enormous portfolio over time without the worry of a tax bill eating into your income.

Next, set up a regular investment plan – sometimes called a monthly savings plan or dividend reinvestment plan.

Most reputable UK investment platforms allow you to pick a handful of funds or investment trusts and automatically buy a fixed pound amount each month.

This approach, known as pound-cost averaging, smooths out the inevitable market fluctuations.

Some months you’ll buy when shares are down, capturing a temporarily higher dividend yield on that slice of your purchase.

Other months the yield will look lower because prices have risen, but your existing holdings will be worth more.

The key is consistency.

The money leaves your current account by direct debit, silently and relentlessly building your future.

I began with a plan that invested £5 a day (£150 a month) into a broad UK dividend income fund, while I learned the ropes.

A fund or investment trust can be a fantastic starting point because it spreads your money across dozens of high-quality UK dividend stocks, giving you instant diversification and a blended dividend yield that’s often in the 3.5%–4.5% range.

You get the income without the stress of picking individual companies from day one.

Once you’re comfortable, you can then start adding selected shares alongside your fund, customising your portfolio’s dividend yield to match your goals.

The current ISA allowance is £20,000 per year, far more than most beginners need, which means you can grow an enormous portfolio over time without the worry of a tax bill eating into your income.

Next, set up a regular investment plan – sometimes called a monthly savings plan or dividend reinvestment plan.

Most reputable UK investment platforms allow you to pick a handful of funds or investment trusts and automatically buy a fixed pound amount each month.

This approach, known as pound-cost averaging, smooths out the inevitable market fluctuations.

Some months you’ll buy when shares are down, capturing a temporarily higher dividend yield on that slice of your purchase.

Other months the yield will look lower because prices have risen, but your existing holdings will be worth more.

The key is consistency.

The money leaves your current account by direct debit, silently and relentlessly building your future.

I began with a plan that invested £5 a day (£150 a month) into a broad UK dividend income fund, while I learned the ropes.

A fund or investment trust can be a fantastic starting point because it spreads your money across dozens of high-quality UK dividend stocks, giving you instant diversification and a blended dividend yield that’s often in the 3.5%–4.5% range.

You get the income without the stress of picking individual companies from day one.

Once you’re comfortable, you can then start adding selected shares alongside your fund, customising your portfolio’s dividend yield to match your goals.

The Dividend Reinvestment Plan: The Quiet Snowball Most People Ignore

If there’s one thing I wish every new investor would see every time they close their eyes, it’s the power of a dividend reinvestment plan, universally known as a DRIP. A DRIP automatically uses your cash dividends to buy more shares of the same company or fund, often with reduced or zero dealing fees. Instead of the £50 dividend landing in your account as cash (where it might quietly get spent on takeaways), it buys little fractions of additional shares.

Those new shares then generate their own dividends next quarter, which buy even more shares. It’s compounding in its purest, most elegant form.

Let’s say you own £10,000 worth of a UK dividend fund with a dividend yield of 4%.

That generates £400 a year in dividends. If you take the cash, next year you’ll still have the same number of shares and you’ll likely get another £400, assuming the dividend stays flat.

If instead you reinvest those dividends and the fund’s yield remains around 4%, you now have £10,400 at work.

The following year, your income is £416. It doesn’t sound seismic in year two, does it?

But carry that forward twenty years, with dividends gently rising and reinvestment continually happening, and the curve goes from a straight line to a steep upward arc.

By the time I turned 23, the annual income being generated by my reinvested dividends had overtaken my contributions.

At that point, my portfolio had essentially hired itself.

I could have stopped adding a single fresh pound and my income would still have grown, funded by the dividend yield generated by shares bought years earlier.

That transition was the moment I realised ordinary retirement age was optional.

Nearly every UK investment platform offers a dividend reinvestment plan.

Check the box when you set up your ISA, and forget about it. Your future self will want to take your present self out for a really good coffee and a slice of cake.

Instead of the £50 dividend landing in your account as cash (where it might quietly get spent on takeaways), it buys little fractions of additional shares.

Those new shares then generate their own dividends next quarter, which buy even more shares. It’s compounding in its purest, most elegant form.

Let’s say you own £10,000 worth of a UK dividend fund with a dividend yield of 4%.

That generates £400 a year in dividends. If you take the cash, next year you’ll still have the same number of shares and you’ll likely get another £400, assuming the dividend stays flat.

If instead you reinvest those dividends and the fund’s yield remains around 4%, you now have £10,400 at work.

The following year, your income is £416. It doesn’t sound seismic in year two, does it?

But carry that forward twenty years, with dividends gently rising and reinvestment continually happening, and the curve goes from a straight line to a steep upward arc.

By the time I turned 23, the annual income being generated by my reinvested dividends had overtaken my contributions.

At that point, my portfolio had essentially hired itself.

I could have stopped adding a single fresh pound and my income would still have grown, funded by the dividend yield generated by shares bought years earlier.

That transition was the moment I realised ordinary retirement age was optional.

Nearly every UK investment platform offers a dividend reinvestment plan.

Check the box when you set up your ISA, and forget about it. Your future self will want to take your present self out for a really good coffee and a slice of cake.

Choosing UK Dividend Stocks That Deliver A Reliable Yield

Eventually, you’ll likely want to add individual UK dividend stocks to your portfolio. This is where the craft gets deeply satisfying. You’re no longer chasing the highest dividend yield on offer... you’re hunting for quality, durability, and a track record of inflation-beating increases.

I look for a few broad characteristics, and I’ll share them, remembering that this is what worked for me and isn’t personal advice.

First, I favour companies that provide things people use every day regardless of the economy – think household goods, energy, insurance, and telecommunications.

These boring giants might not double their share price overnight, but they tend to generate reliable cash flow that funds a steady, growing dividend yield.

In the UK, our market is home to dozens of such firms.

Second, I study the dividend history. A company that has maintained or increased its dividend for five, ten, fifteen, or twenty consecutive years is demonstrating a culture of rewarding shareholders.

Even during downturns, these companies treat the dividend as a sacred promise.

That track record doesn’t guarantee the future, but it tells you what the boardroom prioritises when times get tough.

Third, I re-check the dividend payout ratio and make sure the yield isn’t a fluke caused by a plunging share price.

I also glance at debt levels. A heavily indebted company servicing its loans might be forced to redirect cash away from dividends at the first sign of an issue, wiping out the dividend yield you were counting on.

A balance sheet with moderate, manageable debt is your friend.

Finally, I don’t overcomplicate things.

I hold a core of individual household names that I understand. Some years my portfolio’s overall dividend yield sits at 3.8%... other years it climbs above 5% if I’ve been buying during downturns.

I never let the yield dictate my choices... I let quality dictate my choices, and the yield naturally follows.

You’re no longer chasing the highest dividend yield on offer... you’re hunting for quality, durability, and a track record of inflation-beating increases.

I look for a few broad characteristics, and I’ll share them, remembering that this is what worked for me and isn’t personal advice.

First, I favour companies that provide things people use every day regardless of the economy – think household goods, energy, insurance, and telecommunications.

These boring giants might not double their share price overnight, but they tend to generate reliable cash flow that funds a steady, growing dividend yield.

In the UK, our market is home to dozens of such firms.

Second, I study the dividend history. A company that has maintained or increased its dividend for five, ten, fifteen, or twenty consecutive years is demonstrating a culture of rewarding shareholders.

Even during downturns, these companies treat the dividend as a sacred promise.

That track record doesn’t guarantee the future, but it tells you what the boardroom prioritises when times get tough.

Third, I re-check the dividend payout ratio and make sure the yield isn’t a fluke caused by a plunging share price.

I also glance at debt levels. A heavily indebted company servicing its loans might be forced to redirect cash away from dividends at the first sign of an issue, wiping out the dividend yield you were counting on.

A balance sheet with moderate, manageable debt is your friend.

Finally, I don’t overcomplicate things.

I hold a core of individual household names that I understand. Some years my portfolio’s overall dividend yield sits at 3.8%... other years it climbs above 5% if I’ve been buying during downturns.

I never let the yield dictate my choices... I let quality dictate my choices, and the yield naturally follows.

My Simple Strategy To Build A Stock Market Income Stream You Can Retire On

You might be wondering what blueprint I followed to achieve this by 23. It wasn’t genius... it was behaviour. I committed to treating every pound I invested as an employee whose only job was to find more employees.

My dividend yield focus meant I thought less about “Is the market up today?” and more about “How many shares did my dividends buy while I was asleep?”

The strategy is so simple it almost feels like a cheat code.

First, maximise your tax shelter by using a Stocks and Shares ISA, and if you’re truly thinking long term, consider a Self-Invested Personal Pension (SIPP) for the tax relief, though that ties money up until later in life.

I used an ISA so I could access the income whenever I wanted.

Second, pick a low-cost UK dividend-focused exchange-traded fund or investment trust as your anchor.

This gives you a broad dividend yield without the need to become a stock analyst overnight.

Third, set your DRIP to “on”.

Fourth, increase your monthly contribution whenever your wages rise or you find spare cash.

My rule was that every time I got a pay rise, half of it went straight into my regular investment plan before I ever saw it in my current account.

That painless increase turbocharged my portfolio’s growth.

I also learned to relish market downturns. When the FTSE 100 falls 15% and headlines scream panic, the same high-quality shares are suddenly offering a materially higher dividend yield.

If you’re still in the accumulation phase, a sale is exactly what you want.

My reinvested dividends purchased more shares during those fearful periods than during the exuberant ones.

Remember, your goal isn’t to be the cleverest person in the room.

It’s to own a collection of profitable, cash-generating businesses that collectively drip an ever-growing income into your ISA.

The dividend yield on cost will, with patience, outstrip anything you could have imagined at the start.

I committed to treating every pound I invested as an employee whose only job was to find more employees.

My dividend yield focus meant I thought less about “Is the market up today?” and more about “How many shares did my dividends buy while I was asleep?”

The strategy is so simple it almost feels like a cheat code.

First, maximise your tax shelter by using a Stocks and Shares ISA, and if you’re truly thinking long term, consider a Self-Invested Personal Pension (SIPP) for the tax relief, though that ties money up until later in life.

I used an ISA so I could access the income whenever I wanted.

Second, pick a low-cost UK dividend-focused exchange-traded fund or investment trust as your anchor.

This gives you a broad dividend yield without the need to become a stock analyst overnight.

Third, set your DRIP to “on”.

Fourth, increase your monthly contribution whenever your wages rise or you find spare cash.

My rule was that every time I got a pay rise, half of it went straight into my regular investment plan before I ever saw it in my current account.

That painless increase turbocharged my portfolio’s growth.

I also learned to relish market downturns. When the FTSE 100 falls 15% and headlines scream panic, the same high-quality shares are suddenly offering a materially higher dividend yield.

If you’re still in the accumulation phase, a sale is exactly what you want.

My reinvested dividends purchased more shares during those fearful periods than during the exuberant ones.

Remember, your goal isn’t to be the cleverest person in the room.

It’s to own a collection of profitable, cash-generating businesses that collectively drip an ever-growing income into your ISA.

The dividend yield on cost will, with patience, outstrip anything you could have imagined at the start.

Your First Step Starts Today

I do not have any superpowers. I’m just someone who learned, early, that dividend yield could be a bridge from “I want to retire someday” to “I’m already free”. The very fact you’ve read this far tells me you have the curiosity and the discipline to travel the same path. Your next move couldn’t be simpler. Open a Stocks and Shares ISA with a reputable, low-cost UK provider if you haven’t already. Choose a diversified dividend income fund or investment trust – one that holds dozens of solid UK dividend stocks – and set up a regular monthly direct debit for an amount that feels sustainable, even if it’s just £25. Tick the box for dividend reinvestment. Then, and this is the challenging part, leave it alone. Let the dividend yield work its quiet arithmetic while you get on with living your life. In five years, you’ll be astonished at what’s quietly accumulated. One last thought... ... A decade from now, you will either have started this journey or you won’t. Either way, the time will pass. I chose to let that passing time be filled with dividends compounding, reinvesting, and ultimately replacing my need for a traditional wage. All because I took the time to understand one humble percentage. Now you have that same understanding. The only thing left is to use it.Frequently Asked Questions About Dividend Yield

What is dividend yield in simple terms?

Dividend yield is the annual income you receive from a company's shares, expressed as a percentage of what you paid for them. If you buy a share for £2.00 and it pays 10p in dividends over the year, the yield is 5%. Think of it like the rental yield on a buy-to-let property – it tells you how much cash your investment generates relative to its cost.

How do you calculate dividend yield?

The formula is straightforward: Dividend Yield = (Annual Dividend Per Share ÷ Current Share Price) × 100. For example, if a company pays 20p per share annually and the share price is 400p (£4), the yield is 20 ÷ 400 × 100 = 5%. That means for every £1,000 you invest, you'd expect £50 in annual dividend income.

What's the difference between trailing and forward dividend yield?

Trailing yield looks backwards at what the company paid in the last twelve months. Forward yield looks at what the company expects to pay over the next twelve months. I focus on the forward yield because I'm buying future income, not past income. For a healthy company, the two are usually close – if they're wildly different, that's a clue to investigate.

Why is a high dividend yield often a warning sign?

A sky-high yield can be a trap. If a share price plummets faster than the dividend is reduced, the yield spikes artificially. A beginner sees 20% and piles in, only for the company to suspend the dividend entirely because it's haemorrhaging cash. The yield vanishes, and the investor is left with a heavy capital loss and zero income. This is the classic dividend yield trap.

What is a safe dividend yield range for UK stocks?

A genuinely safe, growing dividend yield usually sits somewhere in the 2%–4.5% range for most healthy UK dividend stocks. Some sectors, like certain renewable infrastructure funds, might offer a reliable 6%–8%, but you must understand why the yield is elevated before buying. I ignore any dividend yield above 7% until I've done at least an afternoon of homework.

What is the dividend payout ratio and why does it matter?

The dividend payout ratio tells you what percentage of a company's profits are being paid out as dividends. If a company earns £100 million and pays out £60 million, the payout ratio is 60% – that feels comfortable. A payout ratio above 100% means the company is paying out more than it earns, often using borrowed money or asset sales. That can't last forever. I generally look for a payout ratio of 60% and below for most mature UK dividend payers.

What is yield on cost and why is it important?

Yield on cost is the dividend yield you get on your original investment, not the current share price. If you bought shares at £1.00 with a 10p dividend, your initial yield was 10%. Five years later, if the dividend grew to 14p, your yield on cost would be 14% – even if the share price had doubled and the current yield to new investors was only 7%. This is where true wealth hides – your money starts working harder than you do.

What is a dividend reinvestment plan (DRIP)?

A dividend reinvestment plan (DRIP) automatically uses your cash dividends to buy more shares of the same company or fund, often with reduced or zero dealing fees. Instead of the dividend landing in your account as cash, it buys little fractions of additional shares. Those new shares then generate their own dividends next quarter, which buy even more shares. It's compounding in its purest, most elegant form.

How do I start dividend investing with a small amount of money?

Open a Stocks and Shares ISA – it shelters all your dividends and capital gains from the taxman. Every pound of dividend yield you generate inside an ISA is yours to keep, completely tax-free. Set up a regular monthly direct debit – even £25 – into a diversified UK dividend fund or investment trust. Tick the box for dividend reinvestment. Then leave it alone. Consistency matters far more than the lump sum.

What characteristics should I look for in UK dividend stocks?

I favour companies that provide things people use every day regardless of the economy – household goods, energy, insurance, and telecommunications. These boring giants generate reliable cash flow. I study the dividend history – a company that has maintained or increased its dividend for five, ten, fifteen, or twenty consecutive years demonstrates a culture of rewarding shareholders. I re-check the payout ratio, glance at debt levels, and never let the yield dictate my choices – I let quality dictate my choices, and the yield naturally follows.

Key Takeaways: Making Dividend Yield Work For You

I’ve thrown a lot of warmth and wisdom at you, so let’s gather the most important bits in one place. These are the principles that shifted me from a wide-eyed teenager to someone financially independent by age 23.| 💡 Key Takeaways |

|---|

| Dividend yield is your compass, not your master – The yield tells you how much income your money buys. Use it to compare opportunities, but never buy a share purely because the yield is high. |

| Check the dividend payout ratio – A safe payout ratio (ideally 60% and below) means the company can comfortably afford its dividend. Ratios over 100% are a red flag. |

| Beware the high dividend yield trap – If a yield looks astronomically high, the share price has probably fallen for a reason. Ask why before you invest. |

| Use the rental property test – Would you buy a house with that yield if you had to manage the tenant and fix the boiler? If the answer is no, think twice. |

| Embrace a dividend reinvestment plan (DRIP) – Let your dividends buy more shares automatically. That quiet compounding is the engine behind every early retiree. |

| Start small, start now, use an ISA – A £25 monthly direct debit into a diversified UK dividend fund inside a tax-free ISA can change your life. The best time to start was years ago... the second-best is today. |

| Focus on yield on cost – The dividend yield you get on your original investment grows over time if the company raises its dividend. That's where true wealth hides. |

| Stay boring, stay consistent – The path to financial independence through dividend investing isn't thrilling. Boring companies, boring plans, beautiful outcomes. |

| Relish market downturns – When the market falls, high-quality shares offer a materially higher dividend yield. If you're in the accumulation phase, a sale is exactly what you want. |

| Your money works harder than you do – Dividends don't ask for permission. They appear in your account automatically, and over time, the income from reinvested dividends can overtake your contributions – making retirement optional. |